“Low volatility could be ‘the quiet before the storm,’” Nobel laureate Robert Shiller told CNBC last week, adding: “I lie awake worrying.” Over the past 20 years, the CBOE Volatility Index (VIX) has closed below 10 on only 21 days, 13 of which have been in the past two months. The current streak of 270-plus days without a 5% drawdown in any of the major U.S. indices is the longest since 1996. Meanwhile, U.S. equity values continue to diverge from earnings — Schiller’s Cyclically Adjusted PE Ratio (CAPE) has only been higher two times in market history: 1929 and 2000.

Yet, despite the many bulls claiming low volatility is historically normal, and therefore not a warning sign, evidence is beginning to mount that U.S. equity markets may be near a volatility-driven tipping point. With the market consolidated (WILTW June 29, 2017) and buoyed by the lowest interest rates in 5,000 years, investors have taken on more and riskier leverage in search of yield. Compounding the risk, much of that leverage has been “justified” by passive strategies pegged to low volatility. As Baupost Group’s Jim Mooney warned last week: “Low volatility would not be a problem if not for strategies that increase leverage when volatility declines.”

If passive strategies have a bias to buy, they can also have a bias to sell — a threat we explored in WILTW June 15, 2017. With hundreds of billions of dollars of investments now linked to volatility, a spike in the VIX could trigger a devastating algorithmic sell cascade.

Time and again in these pages, we have stressed the need to look beyond the U.S. for opportunity. The longer volatility remains low, the more imperative this becomes. It is impossible to pinpoint when the low-volatility regime will end, but as Howard Marks stressed in an Oaktree client letter last week: “It’s better to turn cautious too soon…than too late after the downslide has begun.”

Mooney believes low volatility could be the harbinger of the next financial crisis. Business Insider synopsized his reasoning:

“While leverage is not directly responsible for every financial disaster, it usually can be found near the scene of the crime,” Baupost’s president and head of public investments wrote in the letter. “The lower the volatility, the more risk investors are willing to or, in some cases, required to incur.”

Assets whose performance is linked to volatility include a huge amount of money…These funds, including quant funds and so-called risk parity funds, target a specific level of risk, and when volatility spikes, sending risk upwards, it can trigger selling…

As such, any spike in equity market realized volatility, even to historical average levels, has the potential to drive a significant amount of equity selling (much of it automated). Such selling would, in turn, further increase volatility which would call for more deleveraging and yet more selling.”

Wolf Street’s Wolf Richter pointed out last week that total outstanding leveraged loans in the U.S. reached $943 billion at the end of 2Q17. Moreover, covenant-lite loans — high-risk instruments issued by junk-rated borrowers, with few protections for creditors — made up 72.5% of that total, a record. Yet still, the amount of high-risk leverage in the market is likely even higher. Securities- based loans (SBLs) — or “shadow margin” — are often not disclosed by financial firms, meaning totals remain opaque. However, for the firms that have revealed statistics, growth rates suggest SBLs are also at record highs: Morgan Stanley’s SBLs have doubled since 2013 to $36 billion and Bank of America Merrill Lynch’s SBLs were at $40 billion at the end of 2016, up 140% from 2010.

“Refusal to acknowledge the existence of risk has become a pandemic,” Richter writes. “This of course has been the explicit strategy of the Fed since the Financial Crisis — to push investors out ever farther toward the thin end of the risk branch.”

The meteoric rise of passive strategies — unbeholden to price discovery, endowed with the biases of their creators — has further encouraged investors to ignore risk. Jonathan Jacobson, founder of Highfields Capital Management, wrote in a recent letter to clients about why the increasing influence of quants is obfuscating market risk:

“We are convinced that “quant’ funds”, which have attracted hundreds of billions of dollars in the last few years and a significant portion of which use leverage, and whose models and various strategies are largely based on price action and correlations extracted from the reasonably-recent past when volatility has been low (largely of their own making), have contributed mightily to the illusion that market risk is low. As the money continues to flow into these strategies, this dynamic becomes self-fulfilling.”

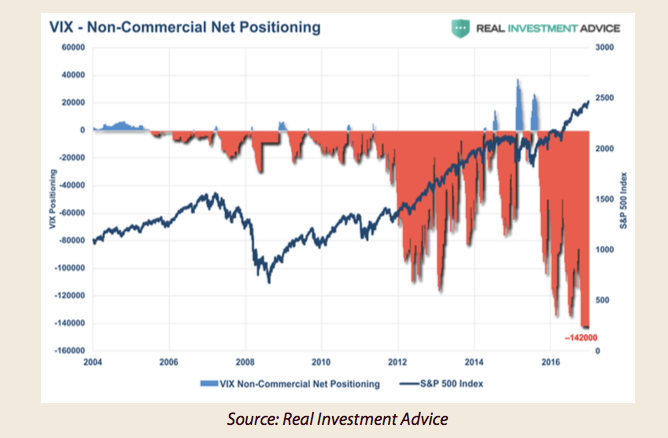

Of course, there’s a flipside to that self-fulfillment. As we wrote back in June about the systemic threat created by passive strategies: “If a key sector failure, a geopolitical crisis, or even an unknown, black box bias pulls an algorithmic risk trigger, will the herd run all at once?” This is Mooney’s point as well: volatility spiking would trigger algorithms to deleverage, thus exacerbating the volatility, leading to even more deleveraging. Compounding the threat, VIX short positioning is at record levels, which could further expedite an unwinding:

So the question is, what could drive a spike in volatility? The obvious answer is central banks normalizing monetary policy. Many assume central bankers are aware unwinding QE could end the low-volatility regime and will act to protect the “new normal”. As history attests, this faith is misguided and dangerous. Yet, even if the majority is correct, that does not mean other volatility catalysts don’t exist.

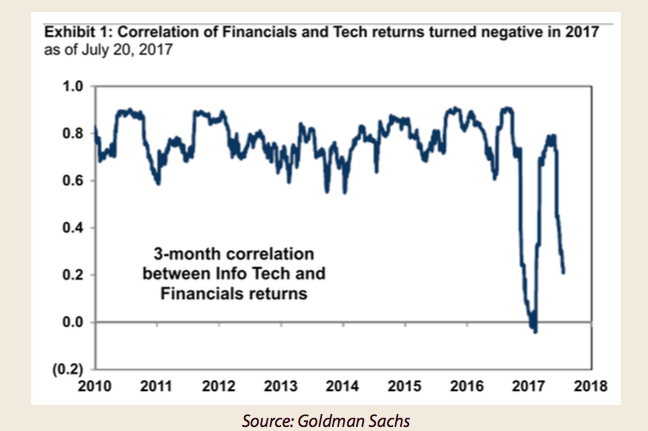

Recently, J.P. Morgan equity derivatives strategist Marko Kolanovic highlighted one such potential catalyst. Financials and tech stocks have been moving in the same direction only 30% of the time of late, in stark contrast to the longer-term norm of 80%:

As CNBC wrote last week, this seesaw dynamic between tech and bank stocks is “happening in the context of an overall market that has become quite selective and eclectic, with stocks and sectors rotating in and out of favor with unusual alacrity.” The consequence is market balance and in turn, low volatility — tech accounts for 23% of the S&P 500 and financials have a 14.5% index weight, meaning they have the power to balance the market as long as one rises as the other one falls.

Citing 1993 and 2000 as evidence — years that saw low volatility and a steep drop in inter-stock correlation eventually return to historical norms — Kolanovic does not believe this divergence-driven stability will last. CNBC recaps his analysis: “It’s generally healthy for individual stocks and sectors to respond independently to incoming fundamental information, when the variation becomes extreme and drives volatility to extreme lows, the market can become unstable and vulnerable to a swift selling storm.”

Seemingly every day for the past two weeks, the VIX has set new records. In a world defined by political turbulence, a time when U.S. markets appear increasingly frothy, when the Fed has a declared intention to unwind QE, the stability appears unnatural — a menacing codependence between financial engineering and greed.

As Goldman Sachs pointed out recently, there have been 14 low-volatility regimes since 1928 and all have required a large shock — namely a war or recession — to end. However, QE and the rise of passive strategies means history may tell us nothing about what’s to come. And the longer volatility remains suppressed, the bigger the leverage bubble grows and the more costly the correction will be once the passive herd is spooked. As Hyman Minsky once said: “The more stable things become and the longer things are stable, the more unstable they will be when the crisis hits.”

Courtesy of 13DResearch

Comments